The Phoenix construction market is in the middle of a pivot that most local contractors haven’t fully recognized yet. For years, Arizona was a speculative new-build machine: master-planned communities, tract housing, commercial strip centers, all driven by population growth and cheap land. That market still exists, but it’s no longer where the real money is moving. The highest-margin work in the Phoenix metro area in 2026 is concentrated in two sectors that require fundamentally different capabilities: green renovation and retrofit projects, and industrial infrastructure driven by the semiconductor and data center boom. Contractors who are still chasing the old playbook are leaving significant revenue on the table. The ones who saw this shift early are winning big, and this episode breaks down exactly how they’re doing it.

Key Takeaways

-

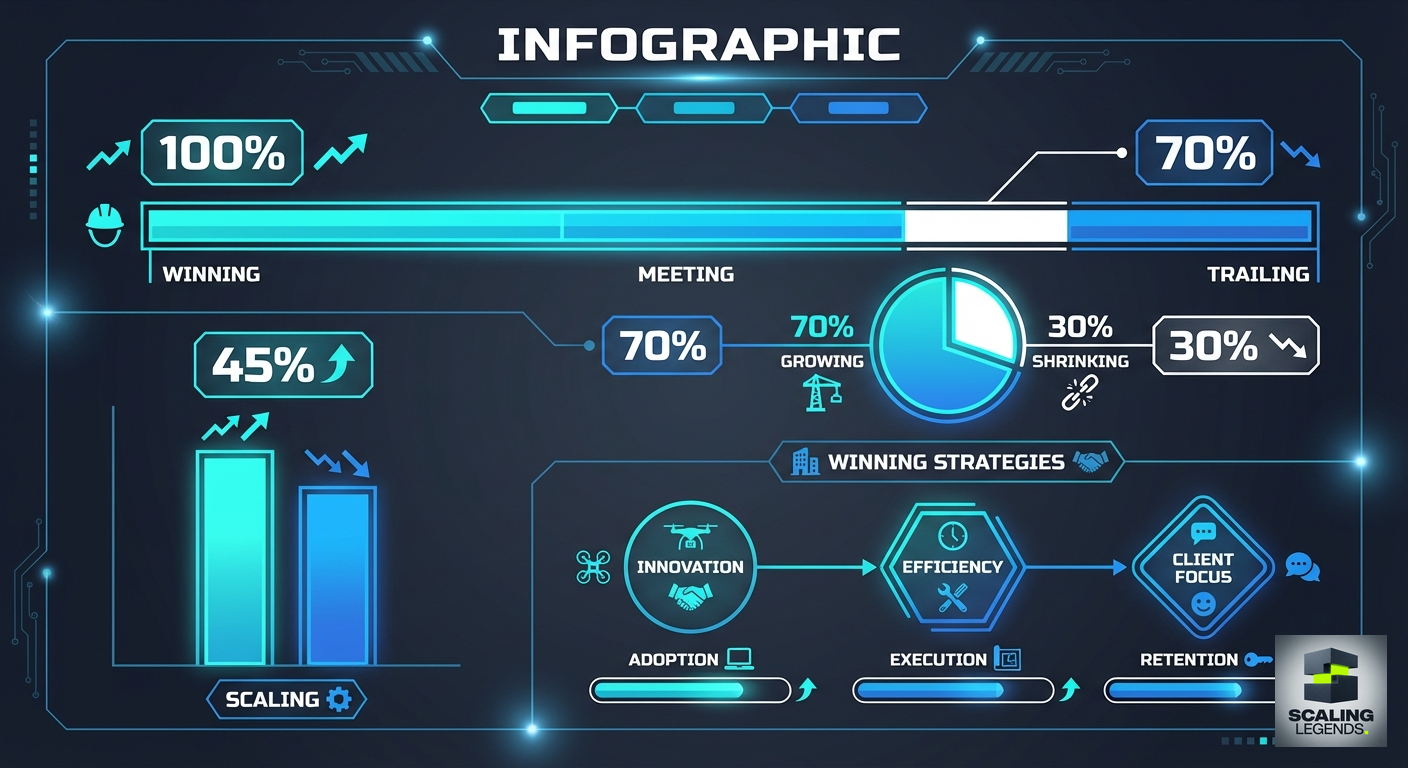

The Market Has Pivoted. Phoenix’s construction spending mix has shifted from 70% new residential / 30% commercial-industrial in 2021 to approximately 45% new residential / 55% commercial-industrial-renovation in 2026, driven by the semiconductor boom and green building mandates.

-

TSMC and Intel Are Reshaping the Valley. Over $65 billion in committed semiconductor facility investment in the Phoenix metro area is creating sustained demand for industrial construction contractors, with project timelines extending through 2030+.

-

Green Renovations Deliver Higher Margins. Contractors specializing in energy efficiency retrofits and green certifications are reporting 12-18% net margins compared to 6-9% on traditional new residential construction in the same market.

-

The Expectation Gap Is the Opportunity. Most Phoenix contractors still think the market wants what it wanted in 2019. The gap between contractor perception and actual market demand creates a competitive opening for firms willing to retool.

-

Water Scarcity Is a Construction Variable. Arizona’s groundwater crisis is adding cost, complexity, and regulatory risk to every construction project, and contractors who understand water-efficient building practices have a genuine differentiator.

-

Industrial Construction Requires Different Skills. Semiconductor fabs and data centers demand cleanroom construction, precision mechanical/electrical work, and quality control standards that residential and light commercial contractors can’t meet without investment in training and equipment.

Arizona’s Shift: From Speculative New Builds to Green Renovations

Between 2015 and 2022, Phoenix was one of the hottest new-build markets in the country. Population growth averaging 1.5% annually, combined with some of the lowest land costs among major metros, fueled a boom in master-planned community development. Contractors who could frame, pour, and finish tract homes at speed built healthy businesses on volume. That era isn’t over, but its dominance is fading. New residential permit activity in the Phoenix metro area has declined approximately 20% from its 2021 peak, and the projects that are getting built are competing on tighter margins as material costs and labor rates have risen faster than home prices.

The smart money is moving toward renovation and retrofit. Arizona’s existing building stock, particularly commercial properties built in the 1990s and 2000s, is aging into a renovation cycle at the same time that energy costs and sustainability mandates are creating demand for green building upgrades. The City of Phoenix adopted updated energy codes in 2024 that significantly increase insulation, HVAC efficiency, and envelope performance requirements for renovated commercial buildings. Maricopa County’s sustainability plan includes incentives for building owners who pursue LEED, ENERGY STAR, or similar certifications during renovations.

For contractors, the economic argument is straightforward. Green renovation projects in the Phoenix metro are delivering 12-18% net margins, compared to 6-9% on traditional new residential construction. The projects are smaller in gross revenue but more profitable per dollar of work. They require specialized knowledge (energy modeling, high-performance HVAC systems, advanced insulation techniques), which creates a barrier to entry that protects margins from pure-price competition. And the demand pipeline is growing, driven by both regulatory requirements and building owners responding to tenant demand for sustainable spaces.

Key Stat: Green renovation contractors in Phoenix are reporting 12-18% net margins compared to 6-9% on traditional new residential work, with the gap widening as energy code requirements tighten.

The contractors who have caught this wave early share a common playbook. They invested in green building certifications for their teams (LEED AP, BPI, RESNET). They built relationships with energy auditors and sustainability consultants who recommend contractors for retrofit projects. And they use project management platforms like Smart Business Automator to track the documentation requirements that green certification programs demand, turning compliance into a selling point for building owners who need certified work.

The Semiconductor and Data Center Boom: TSMC, Intel, and the Industrial Construction Surge

The single largest shift in Phoenix’s construction market has nothing to do with housing. It’s the arrival of advanced semiconductor manufacturing at a scale that’s reshaping the entire Valley’s economy. TSMC’s Arizona campus in north Phoenix represents a $65 billion+ investment across multiple fabrication facilities, with the first fab operational and subsequent phases of construction extending through the end of the decade. Intel’s Chandler campus expansion adds another $20 billion in committed investment. Together, these two projects alone have created more industrial construction demand than Phoenix has seen in its history.

The ripple effects extend far beyond the fab buildings themselves. Every semiconductor facility requires supporting infrastructure: substations and transmission lines for enormous power demands, water treatment and recycling facilities, chemical storage and handling facilities, cleanroom-grade HVAC systems, and miles of ultra-pure piping. Then there’s the secondary construction: worker housing, commercial space for the supplier ecosystem, transportation infrastructure improvements, and community facilities. For contractors in the $5M to $50M range, the subcontracting opportunities on semiconductor projects are substantial and long-duration.

Data centers have followed the semiconductor investment into the Valley. Phoenix has emerged as the second-largest data center market in the US, behind only Northern Virginia. Meta, Microsoft, Google, and a wave of smaller operators have committed to building hyperscale facilities in the West Valley, drawn by lower energy costs (compared to coastal markets), available land, and the infrastructure buildout that semiconductor investment is already funding. The data center construction boom is creating its own labor dynamics, with electricians and mechanical contractors commanding significant premiums.

For traditional residential and light commercial contractors in Phoenix, this industrial surge presents both a threat and an opportunity. The threat is labor competition: semiconductor and data center projects are pulling electricians, plumbers, and HVAC technicians out of the traditional construction labor pool with higher wages, per diems, and overtime opportunities. The opportunity is that contractors willing to invest in the training and equipment needed for industrial work can access projects with longer durations, higher contract values, and more predictable payment schedules than the bid-driven residential market.

How Green Building Certifications Become Profit Centers

Most contractors think of green building certifications as a cost. A fee for the certification process, extra time for documentation, premium materials, and specialized techniques that slow down production. The Phoenix contractors who are winning the expectation gap have flipped this equation. They treat certifications as a profit center, and the math supports them.

Here’s the business case. A typical commercial renovation in Phoenix without any green certification might command a project fee of $150-$200 per square foot. The same project, scoped to achieve LEED Silver or ENERGY STAR certification, commands $180-$240 per square foot. The incremental cost to the contractor (certification fees, additional documentation time, some premium materials) typically runs 5-8% of the project cost. But the incremental revenue is 15-25%. The delta is margin.

Building owners are willing to pay this premium because certified green buildings command higher rents (5-12% premiums in the Phoenix commercial market), lower operating costs (20-35% energy savings), and increasingly, access to favorable financing. PACE (Property Assessed Clean Energy) financing allows building owners to fund energy efficiency improvements through property tax assessments, providing contractors with a built-in financing mechanism that overcomes the “can’t afford the upgrade” objection.

The strategic play for contractors is to own the green certification process, not outsource it. Contractors who employ LEED APs in-house, who can run energy models, and who manage the certification documentation as part of their project delivery are capturing both the construction margin and the consulting margin. This is a significant differentiator in a market where most competitors are still treating green building as a specialty they refer out. Understanding how to position your firm for equipment and capability decisions that support green construction is part of this strategic pivot.

Key Stat: Certified green commercial buildings in Phoenix command 5-12% rent premiums and 20-35% energy savings, creating a willing buyer for contractors who can deliver certified renovation work at competitive prices.

The other piece of the certification-as-profit-center strategy is repeat business. Building owners who see the ROI on one green renovation project tend to roll the approach across their entire portfolio. Contractors who deliver a successful green certification project for a multi-property owner frequently capture follow-on work across 5-10+ additional buildings without competitive bidding. In a market where most contractors are fighting for every project through competitive bids, this kind of relationship-driven pipeline is worth its weight in gold.

The Expectation Gap: What the Market Wants vs. What Contractors Think

The expectation gap is the core thesis of what’s happening in Phoenix’s construction market, and it applies far beyond Arizona. The expectation gap is the distance between what contractors believe the market demands and what the market actually rewards. In Phoenix, that gap is widest in two areas.

First, most contractors still believe that new residential construction is the primary growth market. The data doesn’t support this. While new residential remains a large absolute market, growth rates have flattened and margins have compressed. The growth is in renovation, retrofit, and industrial sectors. Contractors who built their businesses on new residential are reluctant to pivot because the work feels familiar and their teams are configured for it. But familiarity isn’t the same as profitability.

Second, most contractors underestimate the market’s appetite for sustainability. Survey data from the Arizona Chapter of the Associated General Contractors shows that 62% of commercial building owners in the Phoenix metro plan to invest in energy efficiency upgrades within the next three years, driven by rising energy costs, tenant demand, and regulatory requirements. Yet fewer than 15% of local contractors report having any green building capability on their teams. That mismatch is the expectation gap, and it’s creating outsized returns for the firms that have closed it.

Closing the expectation gap doesn’t require a complete business transformation. It requires targeted investments. Sending two or three key team members through LEED AP or BPI certification programs. Building relationships with energy auditing firms and sustainability consultants. Developing case studies from initial green renovation projects that demonstrate capability to future clients. And using data to track market trends, rather than relying on instinct and industry chatter about what’s hot.

The contractors winning in Phoenix right now share a mindset: they let the data tell them where the market is going, rather than assuming the market wants what they’re already set up to deliver. That willingness to follow the data, even when it points away from familiar territory, is the single biggest differentiator between contractors who are growing and those who are stagnating. Tools like Smart Business Automator help contractors track these market signals systematically rather than relying on gut feel and word of mouth.

Water Scarcity: The Construction Variable Nobody’s Pricing Correctly

Arizona’s water crisis is not a future problem. It’s a present reality that is already affecting construction in ways most contractors aren’t accounting for. Groundwater levels in the Phoenix metro area have dropped significantly over the past two decades, and in 2023, Arizona’s governor issued an executive order restricting new assured water supply designations for developments relying on groundwater in Maricopa County. The practical impact: some new developments in the outer suburbs can no longer guarantee the 100-year water supply required for permitting, slowing or killing projects that contractors had in their pipelines.

For contractors, water scarcity shows up in multiple ways. Dust control during construction requires water, and water costs for construction sites in the Valley have increased 25-40% over the past three years. Concrete mixing, equipment washing, and site management all consume water that is becoming more expensive and more regulated. Projects in areas with restricted water access face additional permitting delays and may require on-site water recycling systems that add cost and complexity.

The bigger strategic issue is that water scarcity is reshaping what gets built and where. Developments that can demonstrate water efficiency, whether through xeriscaping, greywater recycling, low-flow fixtures, or alternative cooling systems, have a permitting advantage and a marketing advantage. Contractors who understand water-efficient construction practices and can incorporate them into their project delivery are solving a problem that every developer in Arizona is facing. This is another dimension of the expectation gap: the market increasingly demands water consciousness in construction, and most contractors haven’t caught up.

For industrial projects like semiconductor fabs and data centers, water is an even more critical variable. Semiconductor manufacturing uses enormous quantities of ultra-pure water, and data center cooling systems consume millions of gallons annually. Both TSMC and Intel have committed to building advanced water recycling facilities on their campuses, creating construction demand for specialized water treatment infrastructure. Contractors with experience in water treatment facility construction or industrial-grade water recycling systems have access to a niche market that is growing rapidly and pays well.

Positioning Your Firm for Phoenix’s Next Wave

The Phoenix construction market is not shrinking. It’s transforming. Total construction spending in the Phoenix metro area continues to grow, but the composition of that spending is shifting in ways that reward different capabilities than those that drove success over the past decade. Contractors who position themselves for the next wave need to evaluate their businesses against three questions.

First, do you have green building capability on your team? If the answer is no, the investment required to develop it (certifications, training, energy modeling tools) is modest compared to the revenue opportunity. Start with one or two team members, target a few initial projects to build case studies, and let the results drive expansion.

Second, can you participate in the industrial construction supply chain? You don’t need to bid on a $20 billion semiconductor fab to benefit from the industrial boom. Subcontracting opportunities on semiconductor and data center projects are abundant for firms with the right trade capabilities and safety records. Evaluate whether your existing capabilities (electrical, mechanical, concrete, site work) can translate to industrial applications with targeted training and equipment upgrades.

Third, are you pricing water correctly? This means understanding the true cost of water for your construction operations, incorporating water efficiency into your project proposals, and developing expertise in water-efficient building practices that differentiate your firm from competitors who haven’t adjusted to Arizona’s new water reality.

The contractors winning in Phoenix right now aren’t the biggest or the best-funded. They’re the ones who recognized the expectation gap and moved to close it before their competitors did. The data is clear, the market is shifting, and the firms that adapt will capture outsized returns while those clinging to the old playbook struggle with compressed margins and shrinking backlogs.

Frequently Asked Questions

What is the “expectation gap” in Phoenix construction?

The expectation gap refers to the disconnect between what most Phoenix contractors believe the market demands (primarily new residential construction) and what the market actually rewards (green renovations, industrial infrastructure, and sustainability-focused building). Survey data shows 62% of commercial building owners in the Phoenix metro plan energy efficiency upgrades in the next three years, while fewer than 15% of local contractors report green building capability. This mismatch creates outsized opportunities for contractors who close the gap through targeted investments in certifications, training, and market positioning.

How is the TSMC and Intel semiconductor boom affecting Phoenix contractors?

TSMC and Intel have committed over $85 billion in semiconductor facility investment in the Phoenix metro area, creating the largest industrial construction demand in the region’s history. This affects all contractors in two ways. First, semiconductor and data center projects are pulling skilled tradespeople (especially electricians, plumbers, and HVAC technicians) from the traditional construction labor pool with higher wages and overtime opportunities. Second, the supporting infrastructure these projects require (substations, water treatment, worker housing, commercial development) creates substantial subcontracting opportunities for contractors in the $5M-$50M range willing to invest in industrial-grade capabilities.

Are green building certifications worth the investment for mid-size contractors?

The data strongly supports the investment. Green renovation projects in Phoenix are delivering 12-18% net margins compared to 6-9% on traditional new residential construction. The incremental cost to pursue green certifications (training, documentation, some premium materials) typically runs 5-8% of project cost, while the incremental revenue is 15-25%. Beyond the per-project economics, green certification capability drives repeat business from multi-property owners and creates a competitive moat that protects against pure-price competition. The investment to certify two or three team members typically pays for itself within the first certified project.

How does Arizona’s water scarcity affect construction businesses?

Water scarcity is impacting Arizona construction across multiple dimensions. Water costs for construction sites have increased 25-40% over the past three years. Permitting restrictions on developments relying on groundwater have slowed or killed projects in outer suburban areas. And building owners increasingly demand water-efficient construction practices, creating competitive advantage for contractors who can deliver xeriscaping, greywater recycling, and low-flow systems. For industrial projects like semiconductor fabs and data centers, water treatment facility construction has become a high-demand specialty niche, as these operations consume millions of gallons annually and must build advanced recycling systems to meet regulatory and sustainability commitments.